GenericIrvineResident

New member

Also, real estate gives you pretty great leverage akin to trading options.

You put in 20% of, let's say 1 mil, which is 200k. In one year, if your house appreciates 4% (which is likely in these markets) you can get 40k back from your 200k investment. That's like 20% returns. Obviously, I'm glossing over a lot of things like property taxes etc, but in general you get the idea.

Makes most sense to diversify, though. Invest in stocks/real estate/crypto/etc.

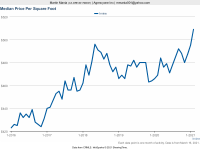

Not everything is about maximizing profits. Everybody needs a home and those that have bought homes in the past have rarely regretted it in the long run.

You put in 20% of, let's say 1 mil, which is 200k. In one year, if your house appreciates 4% (which is likely in these markets) you can get 40k back from your 200k investment. That's like 20% returns. Obviously, I'm glossing over a lot of things like property taxes etc, but in general you get the idea.

Makes most sense to diversify, though. Invest in stocks/real estate/crypto/etc.

Not everything is about maximizing profits. Everybody needs a home and those that have bought homes in the past have rarely regretted it in the long run.

")

")