qwerty

Well-known member

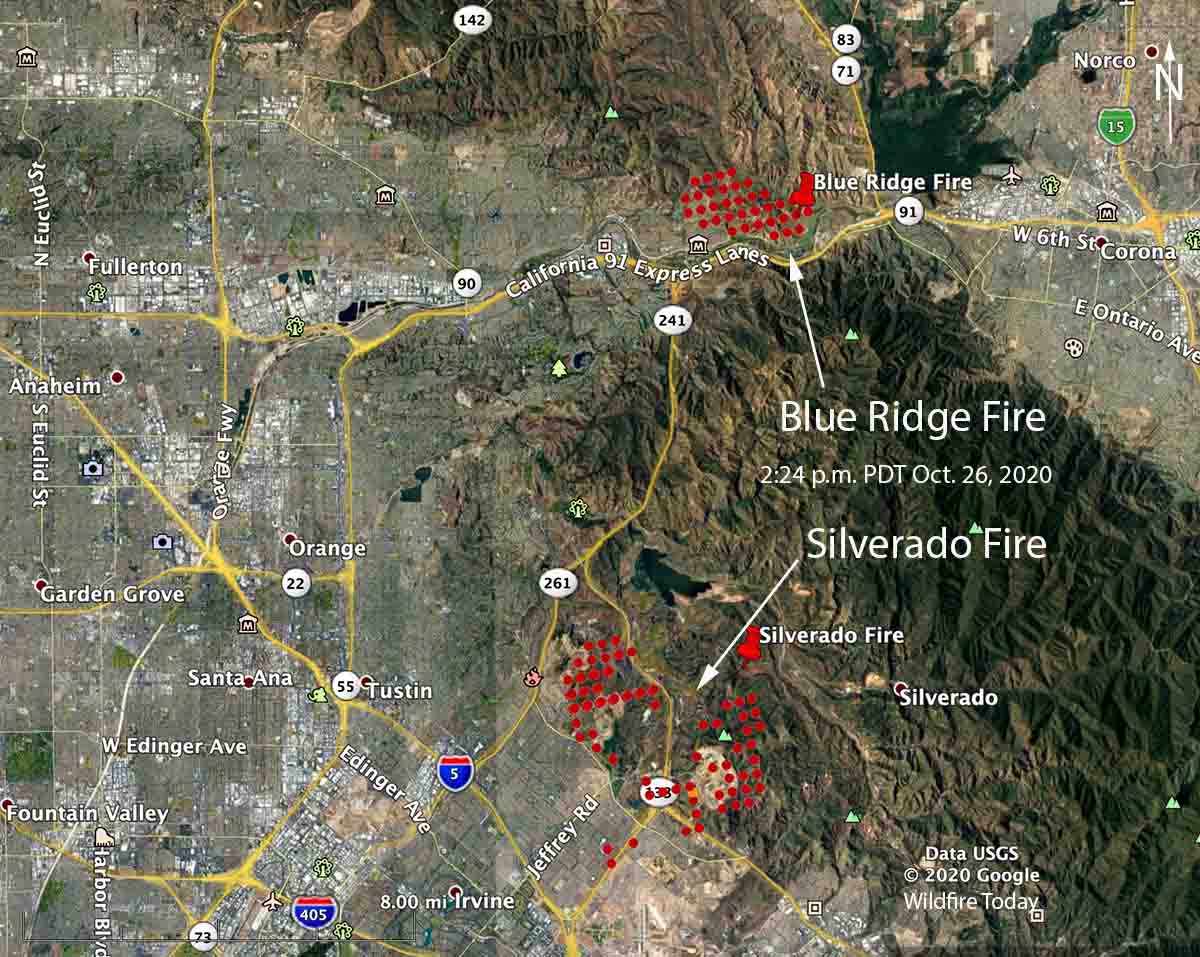

I used to live in Woodbury back in 2008 and a fire burned the area north of portola by sand canyon. If the fire reached there it seems like it will reach portola springs.

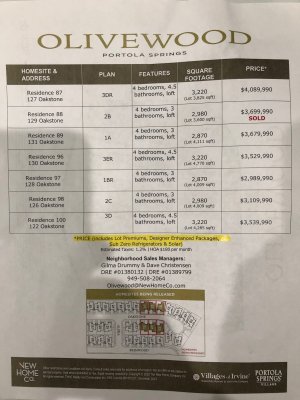

Calbears - do you have other insurance that is covered by your HOA? Is your insurance just for the interior items or does it cover a rebuild of the entire house? That rate is very cheap. I’m pushing 5k a year.

Calbears - do you have other insurance that is covered by your HOA? Is your insurance just for the interior items or does it cover a rebuild of the entire house? That rate is very cheap. I’m pushing 5k a year.