CalBears96

Well-known member

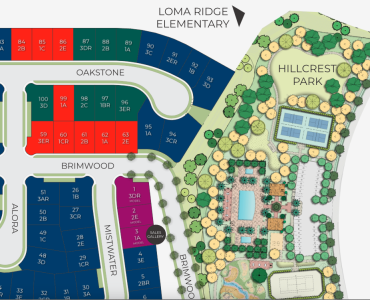

There’s a reason that lot 100 is still on the market. But the latest release was also crazy.Can someone please explain this to me like I'm 5 years old? Why is lot 100 ~$600K more than lot 99? It can't be solely b/c it has one less neighbor, correct?