usctrojancpa

Well-known member

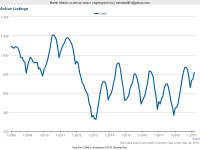

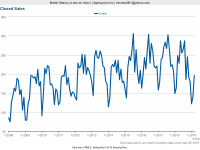

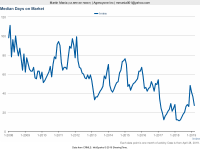

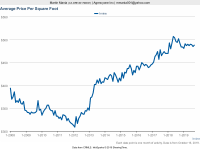

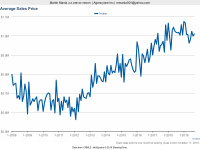

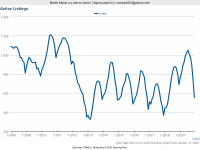

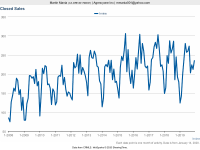

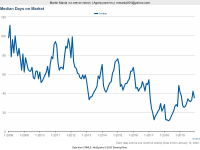

And here are a few 10-year charts to put things into perspective for active listings, home sales, median price per SF, and days on market for all the folks that are more visual. ")

")

irvinehomeowner said:The Closed Sales chart is still looking cyclical to me.

irvinehomeowner said:10 year is good because it covers the last "real" downturn (although may have to expand out to 11 or 12 years).

USCTrojanCPA said:irvinehomeowner said:10 year is good because it covers the last "real" downturn (although may have to expand out to 11 or 12 years).

10 years is as far back as I can capture the data on the graphs and I think it gives a good representation of where things are in comparison during the true buyer's market in 2009-2011.

nosuchreality said:USCTrojanCPA said:irvinehomeowner said:10 year is good because it covers the last "real" downturn (although may have to expand out to 11 or 12 years).

10 years is as far back as I can capture the data on the graphs and I think it gives a good representation of where things are in comparison during the true buyer's market in 2009-2011.

I bought right in the middle of that, JIMHO that was not a buyers market. That was a totally ---ked up market. There weren't a lot of forced sales or weak hands. In fact many of the 'weak' hands were short sales, like we bought, that had multiple people involved, one with a quazi interest in the deal not going thru, one with nothing to lose if it goes south and the prinicpal, the bank, who didn't need to recognize the loss and hit to their until it actually sold.

You could offer the full asking price, in cash and be the highest and only viable offer and the deal wouldn't happen.

Or you hit the other extreme, the home has 22 offers as soon as it was put on the market goes taking back ups, in escrow for month, and back, repeat.

That's not a buyers market.

irvinehomeowner said:@USC:

Can you post your 10-year charts again?

irvinehomeowner said:Can you give us just a median or average sold price?

irvinehomeowner said:Thanks USC!!

Is there an Excel/csv download of the average/median price by month? It's hard to data churn off the chart.

irvinehomeowner said:I have a question, is median price/sft actually better than just looking at median price?

I think it is because it takes into account home size but at the same time, there are other factors that it doesn't cover like room, bathroom count, lot size etc (which median price doesn't cover either).

I remember on the old IHB forums, $/sft was the number everyone was concentrating on.

jamesKirk said:irvinehomeowner said:I have a question, is median price/sft actually better than just looking at median price?

I think it is because it takes into account home size but at the same time, there are other factors that it doesn't cover like room, bathroom count, lot size etc (which median price doesn't cover either).

I remember on the old IHB forums, $/sft was the number everyone was concentrating on.

Yeah this was a hard thing for us to measure since we wanted specific things since we were in the attached condo price range. End unit, two stories, attached 2 car garage. These things are hard to value so you have to find specific examples of sales in the area, which isn?t easy if there only exists a few of that plan in each community since less for sale or sold recently.

Mety said:So early-mid 2018 was the worst time to buy both in terms of the price and the rates.. unless the market picks up and the price goes up in a future.